Chargeback management: How to reduce payment disputes and protect your business

They create additional costs, increase operational workload, and can impact your ability to process payments efficiently in the long term.

What makes chargeback management even more important today is the changing payments landscape. Chargebacks and payment disputes, once primarily associated with card payments, are becoming increasingly relevant across a much broader payment ecosystem.

As a consequence, businesses need to be prepared for a growing range of dispute scenarios.

Effective chargeback management is no longer just about responding to individual cases. It plays an important role in protecting revenue, maintaining operational efficiency, and supporting long-term payment performance.

Why chargeback management is becoming more important

The growing importance of chargeback management is closely linked to changes across the payments landscape.

Buy Now, Pay Later providers such as Klarna, Riverty, but also wallets like PayPal all work with disputes to expand their consumer protection mechanisms.

In the Netherlands, the transition from iDEAL to Wero represents a significant shift. As Wero introduces dispute capabilities that were not previously part of the iDEAL experience, merchants may face new operational requirements and increased exposure to payment disputes.

For merchants, this creates a practical challenge: each payment method may involve different dispute rules, timelines, evidence requirements, and customer expectations. Working with a payment partner that combines payment processing, acquiring, risk expertise, and dispute management tools can help reduce complexity and streamline operations.

What is a chargeback?

A chargeback is a payment dispute initiated by a customer through their bank or payment provider. When a customer believes a transaction was unauthorized, incorrect, or does not meet expectations, they can ask their payment provider or bank to reverse the payment.

A chargeback typically involves multiple parties, including the customer, issuing bank or payment provider, payment network or scheme, acquirer, and merchant.

Chargeback vs refund: What's the difference?

Although they both result in money being returned to the customer, a chargeback and a refund are very different processes.

A refund is initiated by the merchant. It is usually processed after a customer contacts customer support, and both parties agree on a resolution.

A chargeback is initiated by the customer through their bank or payment provider, often without contacting the merchant first. The dispute process involves additional parties, often incurs additional fees or penalties, and requires merchants to provide evidence if they want to challenge the claim.

For this reason, a refund is generally less costly and easier to manage than a chargeback.

Why do chargebacks happen?

Understanding the causes of chargebacks is the first step toward preventing them.

Fraud and unauthorized transactions

One of the most common causes of chargebacks is fraud, including card-not-present fraud, where stolen payment credentials are used without the account holder’s permission. In these cases, customers typically request a chargeback to recover their funds.

Friendly fraud

Not all disputes involve criminal activity. Friendly fraud, also known as first-party fraud, occurs when legitimate customers dispute transactions they have actually authorized. This often happens due to unrecognized billing descriptors, forgotten purchases, or subscription renewals.

According to the 2024 Chargeback Field Report, friendly fraud is now the leading cause of chargebacks, accounting for an estimated 45% of cases.

Delivery issues

Customers expect accurate delivery information and reliable fulfilment.

Late shipments, lost packages, or missing tracking information can lead customers to believe they will never receive their order, increasing the likelihood of a dispute.

Products that don't meet expectations

Poor product descriptions, misleading images, unclear sizing information, or inaccurate specifications can all contribute to dissatisfaction and increase chargeback risk.

Communication breakdowns

When customers cannot easily access support or receive slow responses, they may escalate directly to their bank or payment provider instead of resolving the issue with the merchant.

The true cost of chargebacks

The financial impact of chargebacks continues to grow. A 2025 Mastercard report estimates that the global cost of chargebacks will increase from $33.79 billion in 2025 to $41.69 billion in 2028, highlighting the importance of proactive prevention.

Lost revenue and additional fees

When a chargeback is accepted, merchants often lose both the product and the payment.

Additional fees may also apply depending on the payment method and dispute process.

Operational and administrative costs

Each dispute requires investigation, documentation, and communication. Merchants must collect invoices, shipping details, proof of delivery, and other dispute evidence, which increases operational workload as volumes grow.

Impact on your chargeback ratio

A chargeback ratio measures the percentage of transactions that result in a chargeback over a given period. Payment providers and card schemes closely monitor chargeback ratios.

A high chargeback ratio may indicate fraud, operational issues, or poor customer experience. Over time, excessive dispute rates can result in additional monitoring requirements, penalties or restrictions.

Reputational and business risks

High dispute levels often indicate deeper issues in fraud prevention, fulfilment, or customer experience. Over time, this can affect trust, operational stability, and long-term growth.

How to prevent chargebacks: Best practices for merchants

While chargebacks can never be eliminated completely, merchants can significantly reduce their risk by focusing on prevention.

Set accurate customer expectations

Many disputes originate before the purchase is completed, making pre-purchase communication essential.

Clear product descriptions, high-quality images, accurate dimensions, detailed specifications, and transparent delivery timelines help set expectations from the start.

At the same time, clear refund and return policies should be easy to find and understand, helping customers feel confident about post-purchase outcomes.

The more informed customers are before checkout, the less likely they are to initiate a dispute later.

Provide excellent customer service

Fast, accessible support can prevent many disputes from escalating.

Customers who can quickly resolve issues through customer service are less likely to contact their bank or payment provider. Make it easy for customers to reach your team and respond promptly when problems arise.

Strengthen fraud prevention without hurting conversion

Preventing fraud is essential, but security measures should not create unnecessary friction for legitimate customers.

Modern fraud prevention tools help merchants balance security and customer experience. By reducing the likelihood of unauthorized transactions, they can also help lower chargeback rates and minimize disputes related to payment fraud.

Use 3D Secure 2.2

3D Secure 2.2 adds an additional layer of authentication during checkout.

By supporting methods such as biometric verification, one-time passwords, and risk-based authentication, it helps reduce unauthorized transactions while maintaining a smooth customer experience.

In many cases, successful 3D Secure authentication also enables a liability shift, meaning responsibility for certain fraud-related chargebacks moves from the merchant to the card issuer. As a result, merchants can reduce both their exposure to fraud losses and the number of chargebacks related to unauthorized payments.

Monitor suspicious transactions

Certain patterns may indicate elevated risk.

Unusually large orders, multiple orders on the same address or card, mismatched billing and shipping addresses, multiple payment attempts, or sudden spikes in transaction volume can all warrant additional review.

Proactive monitoring helps identify risky activity before it escalates.

Prepare for peak sales periods

High-volume events such as Black Friday, holiday campaigns, and seasonal promotions can place additional pressure on operations.

Ensuring adequate staffing, inventory visibility, fraud controls, and customer support capacity helps reduce errors that may later result in disputes.

Ensure reliable and traceable deliveries

Tracking information and proof of delivery play a key role in both prevention and resolution.

They provide customers with visibility and merchants with essential dispute evidence.

Improve transaction clarity

Using clear payment descriptors and consistent branding throughout the purchase journey helps customers connect the charge on their statement with the purchase they made, reducing unnecessary disputes.

How to manage chargebacks effectively

Even with strong prevention measures in place, some disputes will still occur.

When they do, having a structured chargeback management process is essential.

- Respond quickly. Chargeback processes are time-sensitive. Merchants typically have a limited window to provide evidence and respond to a dispute. Missing deadlines can result in an automatic loss, regardless of the strength of your case.

- Collect the right evidence. The required dispute evidence varies depending on the reason for the chargeback, but commonly includes invoices, order confirmations, tracking information, proof of delivery, customer communications, and refund records. Keeping this documentation organized makes it easier to respond efficiently and strengthens the ability to challenge disputes through representment when applicable.

- Avoid common mistakes. Some of the most common reasons merchants lose disputes include incomplete responses, missing documentation, late submissions, insufficient evidence. A consistent process helps reduce these risks and improves the likelihood of a successful outcome.

How MultiSafepay helps merchants prevent and manage chargebacks

Managing disputes effectively requires more than reacting when a chargeback arrives. It requires visibility, expertise, and the right technology across the entire payment journey.

As both an acquirer and payment processor, MultiSafepay provides end-to-end control over payment flows, helping merchants improve efficiency and reduce complexity when handling disputes.

Our platform combines risk expertise, integrated technology, and operational tools designed to support both chargeback prevention tools and dispute management across the entire lifecycle.

This is how we support our merchants:

Continuous monitoring and risk expertise

Our dedicated Risk team continuously monitors transaction activity to identify suspicious patterns and support fraud prevention efforts.

By combining global transaction data, advanced risk models, and real-time monitoring, we help merchants reduce exposure to fraudulent activity before it results in disputes.

Built-in tools for chargeback prevention

Security technologies such as 3D Secure 2.2 are fully integrated into our platform, helping merchants strengthen authentication while maintaining conversion rates.

Advanced payment optimization, transaction routing, and risk analysis tools further support both security and payment performance.

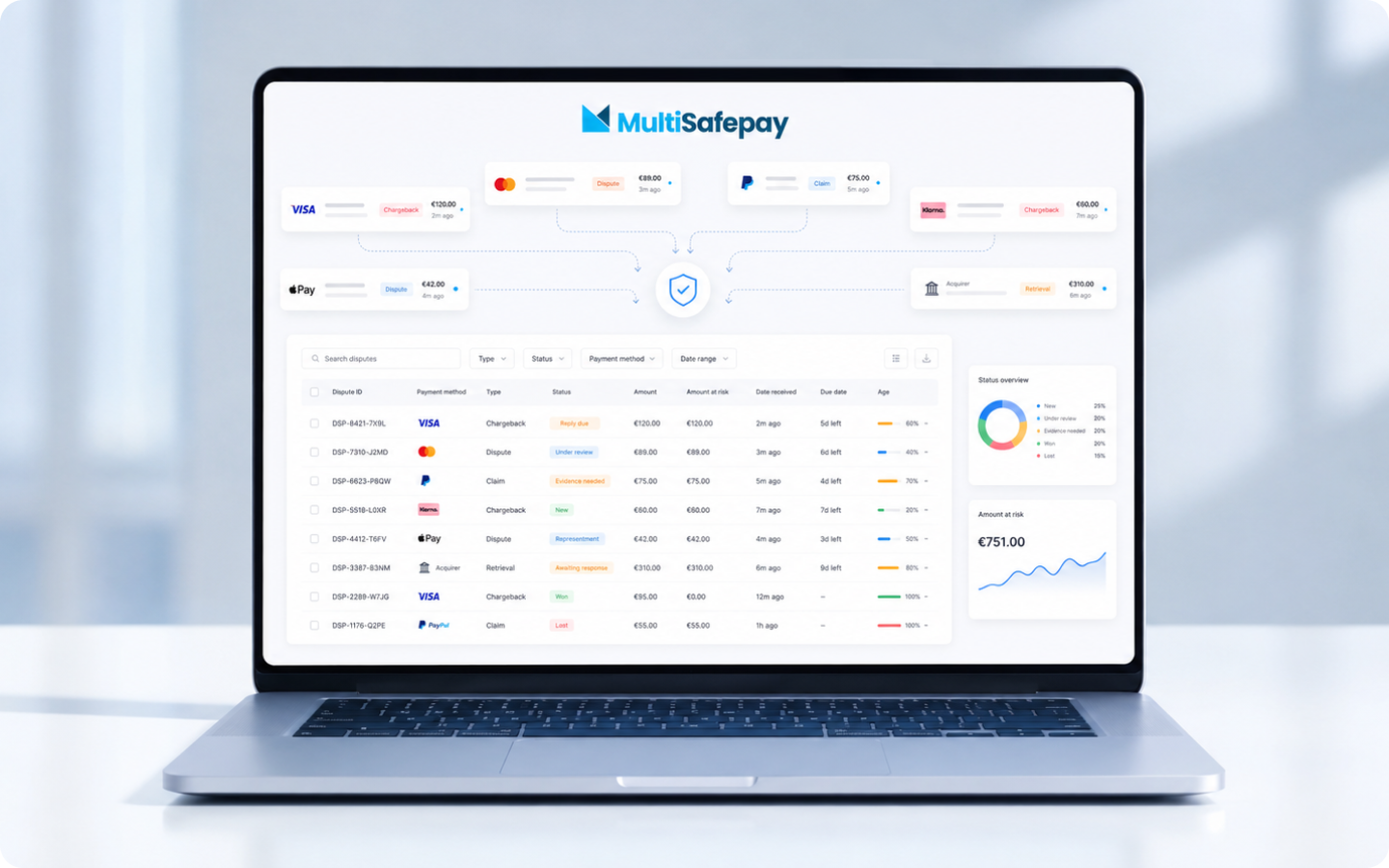

Centralized dispute management

Through the MultiSafepay dashboard, merchants can monitor chargeback activity, track dispute status, and access a centralized overview of new, pending, and disputed cases.

When a dispute needs to be challenged, supporting documents such as invoices, tracking information, proof of delivery, and customer communications can be uploaded directly through the platform.

Dedicated support when it matters

Chargeback processes can be complex, especially as payment methods continue to evolve.

Our teams support merchants throughout the dispute process, helping them understand requirements, submit evidence correctly, and manage cases more efficiently.

By combining fraud prevention tools, payment optimisation, operational visibility, and expert support, MultiSafepay helps merchants reduce chargeback exposure and improve overall payment performance.

Chargebacks can't be eliminated, but they can be controlled

Every growing business will encounter payment disputes at some point. The difference lies in how prepared you are to prevent them and how you respond when they do.

With the right technology and the right payment partner, chargeback management becomes a proactive process rather than a reactive one.

At MultiSafepay, we clear the way, so merchants can focus on growth. From offering more than 40 payment methods to security and compliance, we provide the expertise and technology businesses need to grow with confidence.