What is a merchant acquirer? Acquiring, processing and how they work together

Most merchants never see any of it. But understanding who's doing what, and who's looking out for your business, that makes a real difference to your approval rates, your settlements, and your costs.

Not all payment providers are equal. Many route your transactions through third-party acquirers, adding layers between you and your money. At MultiSafepay, we act as both acquirer and processor, which means fewer hands in the chain and more control where it counts.

So, let's break it down clearly: what is merchant acquiring, how does it relate to payment processing, and why does it matter who you work with

The players in every card transaction

Before we get into merchant acquiring specifically, it helps to understand the key parties involved in any card payment.

The merchant — that's you. You're selling goods or services and accepting card payments from your customers.

The cardholder — your customer, the person whose bank issued the card they're paying with.

The issuer — the bank or financial institution that issued the card to your customer.

The card scheme — networks like Visa and Mastercard that set the rules and route transaction data between banks.

The acquirer — the financial institution that processes card payments on your behalf. The acquirer holds your merchant account, communicates with card schemes and issuing banks, and ultimately ensures funds land in your account.

The payment processor — the technical engine that transmits transaction data between all the parties above.

These roles don't always sit with different companies. In fact, working with a provider that combines them is one of the biggest advantages available to merchants today.

What is a merchant acquirer?

A merchant acquirer (also called an acquiring bank) is a licensed financial institution that enables businesses to accept card payments. To do that, the acquirer establishes and maintains your merchant account, submits transaction requests to the relevant card schemes and issuing banks, handles settlement (moving approved funds into your account) and takes on the financial and compliance risk associated with your transactions, including chargebacks and disputes.

Without an acquirer, you simply can't accept card payments. They're the licensed party that connects you to the card networks.

What is a payment processor?

A payment processor handles the technical side of moving transaction data. When your customer uses their card or enters their details online, the processor captures that data and routes it to the right places — the acquirer, the card scheme, and the issuing bank — to get an approval or decline back to you in seconds. Together, the processor and acquirer also handle clearing and settlement, confirming transaction details and ensuring funds reach your account accurately and on time.

The processor ensures data is transmitted securely, helps manage compliance requirements like PCI DSS, and keeps the technical infrastructure running smoothly.

In traditional setups, the acquirer and processor are separate businesses. You'd have one contract with your acquirer and another with your processor, and they'd communicate through the card networks. That means more relationships to manage, more potential points of failure, and no single partner accountable for the full picture.

Merchant acquirer vs payment processor: What's the difference?

The simplest way to think about it is the acquirer owns the financial relationship, while the processor owns the technical one.

The acquirer is responsible for underwriting your merchant account, settling funds, managing chargebacks, and maintaining scheme compliance. The processor is responsible for routing transaction data securely and quickly between all parties.

In practice, many modern payment service providers combine both functions, which is exactly what MultiSafepay does.

Inside the acquiring process: The 5 steps

Here's what actually happens every time one of your customers pays by card.

1. Checkout

Your customer enters their card details or approves the payment through their digital wallet. This starts the payment process and sends the transaction data to the payment processor.

2. Authentication

The payment request is sent to the card scheme and on to the issuing bank to verify the customer's identity. For certain transactions, the issuer may trigger 3D Secure — a one-time passcode or biometric check — to confirm it's genuinely the cardholder making the purchase.

Strong Customer Authentication (SCA) is a PSD2 requirement across Europe, designed to reduce fraud. Done well, it barely interrupts the customer journey. Done poorly, it creates unnecessary drop-off at the point of payment. Smart exemptions, for low-risk transactions and recognized devices, keep things moving without compromising security.

3. Authorization

The issuing bank checks whether the card is valid, funds are available, and whether there are any fraud signals it needs to act on. At the same time, the acquirer runs its own risk checks alongside the card scheme. This is also where payment success strategies, such as smart routing, retries, and exemption handling, can improve conversion based on issuer preferences.

4. Clearing

Once the transaction is authorized, payment details travel back through the card scheme and issuer to confirm they match the original authorization. Card scheme fees are calculated at this stage based on the data provided, such as card type, region, transaction context, and more.

5. Settlement

This is when money actually moves. Fees are deducted at each stage, and the remaining funds travel from the issuing bank, through the scheme and the acquirer, into your merchant account. Clear reconciliation at this stage means you can see exactly what came in and what was deducted — no surprises.

How card fees work

When you accept a card payment, the transaction fee is split between three parties: the issuer, the card scheme, and the acquirer. How those fees are presented to you depends on your agreement:

Blended pricing gives you a single, fixed rate per transaction — simple and predictable, but with no visibility into the underlying cost breakdown.

Interchange++ pricing breaks the fee down into its three components: the interchange fee (paid to the issuer), the scheme fee, and the acquirer margin. It requires a bit more understanding but gives you full transparency and the ability to optimize over time.

Why working with a direct acquirer matters

Many businesses work with a payment service provider that acts as an intermediary — routing transactions through a third-party acquirer. That means more layers between you and your payments, slower settlements, and less control when something goes wrong.

As a licensed acquirer and processor, MultiSafepay handles both roles directly. That means:

Faster settlements. As a direct acquirer and processor, we control the settlement process end-to-end. No third parties, no waiting.

Lower costs. Removing intermediary acquirers means removing the fees that come with them.

Higher approval rates. Our approval rates consistently run 2–3 percentage points above market, independently benchmarked by Mastercard across our European markets.

More shoppers clear 3D Secure. Smart exemption handling and risk-based authentication mean fewer customers drop off at the authentication step.

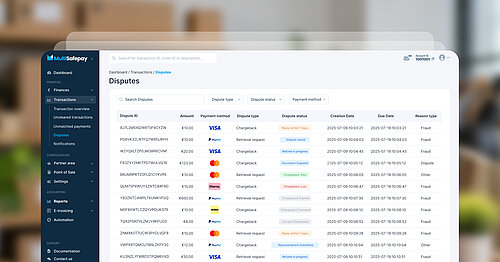

Lower disputes and chargebacks — handled. Our dispute rates run well below market averages, a result of how we manage fraud prevention, risk, and scheme compliance directly. When a chargeback does occur, we help you track it, gather evidence, and manage the process, so you can focus on your customers, not the paperwork.

99.9% uptime. Our infrastructure runs across multiple data centers with instant failover, so your payments keep running even if something goes wrong.

Advanced acquiring and processing. Smart routing and exemption management work together to recover payments, improve conversion, and keep checkout moving.

One integration. Every channel. Real control.

Payments are complex enough without having to manage multiple providers, chase different support teams, or reconcile data across disconnected systems.

At MultiSafepay, we've built our platform in-house, which means every part of the acquiring and processing chain is connected, optimized, and supported by people who actually know how it works. With 40+ payment methods across markets, local teams in the Netherlands, Belgium, Spain and Italy, and direct support, we're set up to help merchants and platforms of every size compete with confidence.

Whether you're selling online, in-store, or across borders, the goal is the same: payments that run smoothly, conversions that climb, and settlements that arrive on time.

That's what it looks like when your acquirer and processor are working as one.

Payments are complex. Your provider shouldn't make them more so. Explore our online payment solutions and see how MultiSafepay can help your business grow.